Personal Finance ・Budgeting

How to Get Out of Debt Quickly: Genius 5-Step Strategy

By: A. Gokkul

Table of Contents

I am so sorry to see you here….

Why?

You clicked on the Pin to read this post; It means there are huge chances that you are struggling to get out of debt and looking for some smart ways to get rid of it.

“Congratulations, you are at the right place.”

I’ve been where you are, staring at credit card balances, loan payments, and bills piling up, wondering how the heck I’d ever break free. Drowning in debt feels like quicksand; the harder you fight, the deeper you sink. The stress kept me up at night and made me feel stuck in a never-ending cycle. After spending countless hours researching on the internet about how to get out of debt, I found a way out.

I created a simple 5-step plan that helped me crush my debt faster than I ever thought possible. Which I will share with you in just a moment….Please keep reading.

But here’s the truth: getting out doesn’t have to take decades.

The steps that I am going to share with you aren’t just theory; they are the exact moves that can help you finally breathe easy and start building real financial freedom.

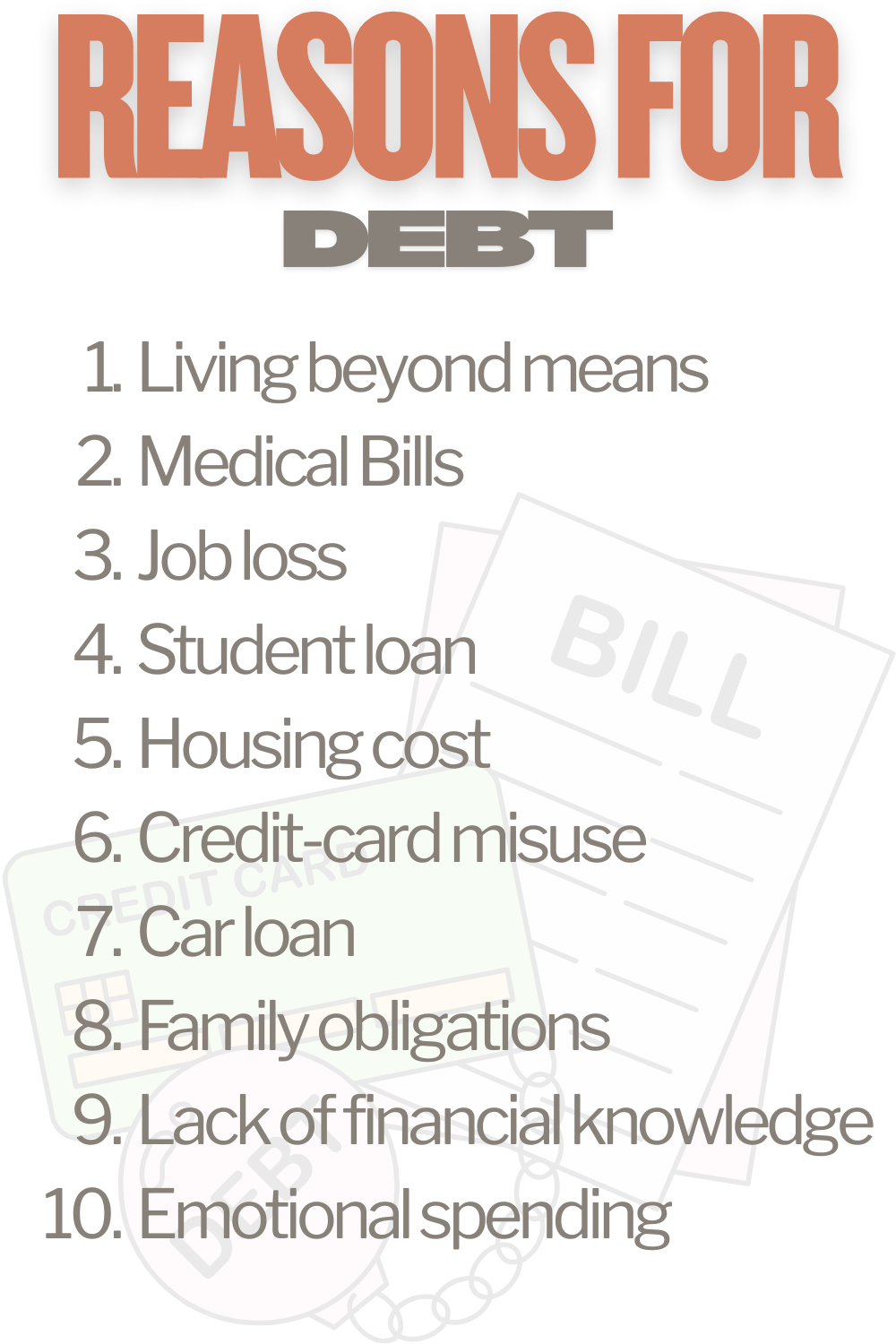

First of all…let’s see why we accumulate debt in our lives. There are many varieties of people out there, so there are a variety of reasons why a person collects debt.

1. Living Beyond Their Means: Keeping up can cost more than you think. Many people overspend to maintain a lifestyle they can’t afford, relying on credit cards to cover daily expenses, and the pressure from peers traps them in growing debt and financial stress.

2. Unexpected Medical Expenses: Medical bills shouldn’t feel like a second emergency. In the US, even with insurance, sudden treatments or ongoing care can cost thousands, and high deductibles, co-pays, and pharmacy bills can quickly push families into financial stress.

3. Student Loans: Student debt: the diploma you didn’t bargain for. Graduates often leave school swamped with loans, and with interest piling up while jobs remain hard to find.

4. Housing Costs: A roof over your head costs more than peace of mind. Oversized mortgages, pricey insurance, steep rent, and endless repairs are a wallet drainer, which makes housing one of the biggest financial burdens families face.

5. Credit Card Misuse: “Swipe now, stress later?” Making only minimum payments, this mentality traps people in a cycle of piling debt that makes it almost impossible to escape.

6. Car Loans or Leasing: Dream car turns into a debt car… Many buy vehicles beyond their budget, rolling negative equity into new loans, and watch interest and depreciation pile up, which leaves them paying far more than the car is worth.

7. Family Obligations: Family comes first, but it can come with a price. Supporting kids or aging parents, navigating divorce costs, or running a household on one income can stretch finances to the breaking point.

8. Poor Financial Planning or Lack of Knowledge: Flying blind with your finances can be costly. Failing to budget, skipping emergency savings, and misunderstanding interest rates or loan terms can quickly lead to unseen money troubles.

9. Impulsive or Emotional Spending: Retail therapy comes with a hidden price. Shopping to cope with stress or sadness, splurging during emotional highs, most of the time, people get into FOMO, which later quickly turns spending into a financial headache.

10. Job Loss or Reduced Income: Life’s paycheck surprises can hit hard. Whether it’s a layoff, company closure, or gaps between freelance work, losing a steady income can make bills overwhelming, often pushing people to rely on credit cards just to get by.

Now, let’s dive into the “Game Plan”.

Step 1: Know Exactly What You Owe

Clarity is the power; You can’t fix what you’re not willing to look at.

You’ve got to face the numbers. Grab a notebook or open a new spreadsheet and write down every single debt you’ve got. I’m talking about everything, credit cards, student loan, car loan, payday loans, personal loan, and if any money is borrowed from your friend, neighbour, or relatives.

For each one, jot down how much you owe, the interest rate, the minimum payment each month, and most importantly, when it’s due. “I can feel you”. This step feels scary, but trust me, you will feel more in control once it’s all laid out in front of you.

Step 2: Build a Budget That Works for You

Next, you need to create a realistic, no-fluff budget.

Look at your monthly income and essential expenses, like rent, groceries, utilities, and transportation. Then, look for your recurring expenses to cut back on. It can be subscriptions you can breathe without, frequent eating outs, random late-night “Amazon buys”, these leaks that keep you in the cycle.

Now here’s the key: every dollar left over should have a job, and if you’re serious about getting out of debt, a big part of that job is going toward your debt payoff plan.

If you find difficult to stick to your budget, which many people do. Find my post here on “how to stick to your budget.”

Step 3: Pick a Debt Payoff Method and Stick to It

Now that you know what you owe and what you can afford to pay, it’s time to choose your game plan.

You’ve got two solid options:

∗ Snowball Method: You start with the smallest debt and pay it off first. This gives you a quick win and motivation to keep going.

∗ Avalanche Method: You start with the debt that has the highest interest rate. This saves you more money in the long run.

Choose the one that feels right for you and stick with it. Don’t bounce between the two. Momentum matters more than perfection.

I suggest. Before choosing from the above methods, clear the debts if you owe to your peers, because that will save your relationship with them, and it really matters.

Step 4: Find Ways to Increase Your Income

I’ll be real with you, budgeting alone won’t always get you there fast enough. That’s why step four is all about bringing in extra cash.

Could you take on a few hours of Uber, DoorDash, or freelance work each week? Maybe sell stuff around the house? Even a few hundred extra bucks a month can really speed things up.

And if you get a tax refund, bonus, or even birthday money, “throw it at your debt.” Think of it like buying your freedom back.

Step 5: Build a Small Emergency Fund & Stay on Track

Here’s the final and super important step.

Before you go all-in on debt payoff, make sure you’ve got at least $500 to $1,000 set aside in a simple savings account. Why? Because life happens. Car repairs, doctor bills, job hiccups, those unexpected things are the reason people fall back into the debt payoff time period.

Once that emergency fund is set, keep your head down, track your progress monthly, and don’t forget to celebrate small wins (without spending, of course).

Final Words

Listen, getting out of debt isn’t just about money, it’s about peace of mind. It’s about freedom. Every payment you make is a step closer to the life you want.

Stick to the plan. Give it time. And don’t quit, even if you mess up a little along the way. You’ve got this.